| Newsmore | ||||||

|

| Culturemore | ||||||

|

| Tourismmore | ||||||

|

| Economymore | ||||||

|

| Lifemore | ||||||

|

| Around Chinamore | ||||||

|

| Newsmore | ||||||

|

| Culturemore | ||||||

|

| Tourismmore | ||||||

|

| Economymore | ||||||

|

| Lifemore | ||||||

|

| Around Chinamore | ||||||

|

| Economy |

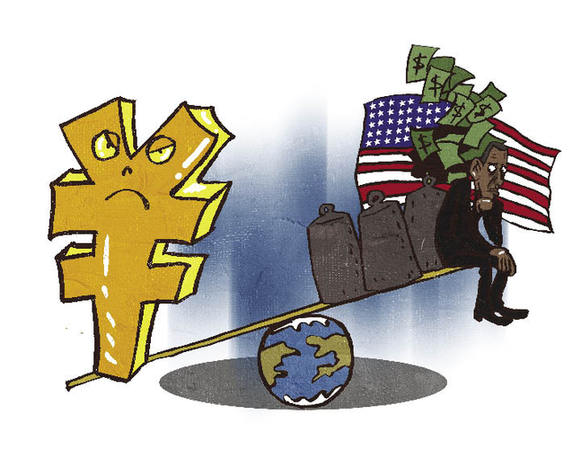

| Wrong Model, Wrong Solution A Chinese scholar challenges C. Fred Bergsten’s model that calculates RMB as being undervalued by 41 percent against the dollar. By staff reporter LIU QIONG

C. Fred Bergsten, director of the Peterson Institute for International Economics, is a notable on Capitol Hill. He is often seen testifying before U.S. Congressional committees and is influential with decisionmakers crafting America’s financial and foreign policies. Earlier this year Dr. Bergsten told the Congress that his calculation showed Renminbi (RMB), or yuan, was undervalued by as much as 41 percent against the dollar. This statement has since been repeated on many occasions by American officials as well as by Paul Krugman, the Nobel laureate economist. However, he is challenged by Zhang Yongjun, a research fellow with the China Center for International Economic Exchanges (CCIEE), China’s “super think tank.” Undervaluation by 41 Percent? According to a report released last year by the Peterson Institute, the U.S. dollar “has been seriously overestimated,” mainly against the RMB and other Asian currencies. The institute noted that among the 25 currencies in their study, most need to get stronger against the U.S. dollars, especially in the case of the RMB, whose value should be significantly increased. “The calculation of 41 percent by the Peterson Institute is widely quoted around the world. It even fueled the recent debates between China and the U.S. on the exchange rate and has placed great appreciation pressure on the RMB,” Zhang said during a monthly economic forum hosted by the CCIEE on April 21, 2010. Zhang refuted Bergsten’s computing model – symmetric matrix inversion method (SMIM) – as being marred in five major aspects. First, it treats the current account equilibrium as the sole exchange rate target. Second, its assumptions of the relevant countries’ current account equilibrium targets are unfounded. Third, it ties the export price elasticity to the exchange rate only, failing to take into account factors such as domestic production costs and product competitiveness. Fourth, it assumes unreasonably that the movement of exchange rates affects exports only, but not imports. And finally, its computation of export price elasticity is oversimplified, as being decided by export ratios only. Therefore, Zhang told those attending the economic forum that Bergsten’s conclusions based upon his model are untenable. Zhang noted that recently the international community, especially the U.S., pushed up their pressure on China to increase the value of the RMB. Though the reasons they cited varied, the core argument was common: China has a large surplus on its current accounts. “There are differences among countries in terms of resources, manpower, technology, culture and capital. Not surprisingly, the countries with comparative advantages in certain aspects can obtain current account surpluses,” Zhang explained, citing several examples. The Middle East and Russia are rich in petrol, Japan and Germany are well-known for their superior manufacturing technologies, and China has the capacity for large-scale manufacturing. Ignoring such differences while simply pursuing a balance of trade among countries would undoubtedly cause a reversal in the trend towards globalization. “Factors impacting the international trade balance are much more complicated than just the exchange rate,” Zhang asserted, adding that domestic demands and economic structures of any two countries would also cause a trade gap between them. “The exchange rate, of course, is one of the variables, but its sway varies for different countries. Therefore, adjusting the rate is not a workable and effective way to erase the bilateral trade imbalance.” Zhang suggests that China modify its domestic demand structure to address its surplus in foreign trade; but he points out that the adjustment should parallel China’s development level, since the structure of domestic demand hinges not only on a country’s economic structure, but also that of various production factors, such as the compositions of the population and labor force. Appreciation Is Not the Solution It is Zhang’s belief that even if the value of RMB is raised against the dollar, Chinese consumers would hardly turn to purchasing more American products, since most of the world’s manufactured goods are produced in China; and if industries are to relocate outside of China to escape the increased production costs caused by the appreciation, they would move to other developing countries and regions instead of to the U.S. In other words, the appreciation of the RMB would not stimulate the creation of jobs in the U.S., whose re-industrialization is a level higher, and cannot improve America’s current accounts. “The development of the world economy has proven that relying on the adjustment of exchange rates cannot remove bilateral trade imbalances,” said Zhang. He cited the examples that the appreciation of the Japanese Yen and German Mark in the late 1980s against the U.S. dollar did not eliminate the two countries’ surplus on their current accounts against the U.S. Wei Jianguo, another economist with the CCIEE, agrees with Zhang, pointing out that the China-U.S. trade imbalance is caused by many factors. On China’s side, around 40 percent of the bilateral trade is general trade and over 50 percent is processing trade. In general trade, China and the United States maintain a relation in which cooperation is greater than competition, for they play different roles in the international division of labor; Chinese exports to the U.S. are concentrated in labor-intensive industries. In processing trade the transnational corporations, including American companies, are taking advantage of China’s less expensive labor costs, which cannot be duplicated in the U.S. On the other side, the U.S. continues to report lower levels of domestic savings and higher consumption rates as Americans have become used to a lifestyle based upon over-consumption. Meanwhile, American products are not more competitive than those produced in Europe or Japan. In 2009 Japan’s exports to China exceeded US $130 billion, while the U.S. exports to China were merely US $69.6 billion. What’s more, the U.S. imposes strict limits on its exports to China, especially for high-tech products. The practice dates to the Coordinating Committee on Export Control from the Cold War and continued into the 1990s, when a series of regulations were implemented to limit exports to China and 18 other countries. In 2007 more U.S. export restrictions were enforced, particularly on China. Furthermore, the U.S. government has introduced additional measures to protect trade, which not only hinders the growth of trade partners, but also shackles its own development. The Lessons of the Yen and Mark Since the 1980s many countries experienced a rapid rise in exchange rates prior to economic crisis. For developed and developing countries alike, when the process of currency appreciation doesn’t come in line with levels of economic development, an economic slump is on the way. Consider the crisis in Greece for example. Since joining the Euro bloc in 1999 Greece has seen a steep gain in its exchange rate, resulting in its current predicament. Other examples include the Sterling crisis in 1992 as well as a financial meltdown in the Nordic countries around 1990. Both were caused by an over-appreciation of exchange rates that led to a domestic economic recession. Zhang also compares the impact of the Yen’s appreciation with that of the Mark to show that different currency policies responding to currency appreciation resulted in differing impacts upon economic development. During the decade starting in 1985 both the Yen and Mark appreciated rapidly. In the case of Japan, its exchange rate was already on the high side in 1985, which meant there was little-to-no room for a continuing rise; but Germany’s rate was not as high. In addition, Japan kept its interest rate at a very low level much longer than Germany, contributing to bubbles in its real estate and stock markets. These factors resulted in the differences between the two giant economies – Japan lost a decade of economic progress while Germany, even though several problems emerged, saw a recovery following its reunification and went on to maintain a healthy pace of development. “We can learn from Germany’s experience though China has a different situation,” noted Zong Liang, director of International Financial Research Center, Bank of China.

|

| VOL.59 NO.12 December 2010 | Advertise on Site | Contact Us |