RMB Internationalization: New Bright Spot in World Economy

The widening usage of China’s currency, the RMB, in international trade and investment has strengthened the country’s trade ties with the rest of the world and actively promoted the growth of the global economy. China has also taken the RMB’s internationalization as an opportunity to promote its exchange rate reform and to open up the country’s capital account.

A Rising International Currency

The RMB is beginning to internationalize under unique historical conditions. Roberto Rigobon, professor of International Macroeconomics at MIT’s Sloan School of Management, identifies six preconditions which are key for a country’s currency to acquire worldwide reputation and international convertibility. These factors include a decent economic scale, stable macroeconomic policies, an open capital account, a flexible exchange rate regime, a mature capital market and positive network externalities. In at least three of these areas – capital account, exchange rate regime and capital market, Rigobon says, the RMB is not yet ready to develop into a world currency.

As a major trading country, China followed the convention of paying US dollars in international trade. However, with the sudden financial collapse of 2008 the dollar’s liquidity shrank, weakening cross-border trade. As a result, in July 2009, China’s State Council announced a pilot program for cross-border trading in RMB. It began in four cities, and was quickly expanded to 20 provinces/autonomous regions and municipalities. In January 2011, China announced that its qualified enterprises and banks could settle their overseas direct investment in RMB, a scheme that was later extended to include all importers and exporters.

The RMB has been increasingly favored in trade with foreign countries and is now the second-most used currency in overseas transactions. By 2013, total cross-border trade settled in yuan hit RMB 5.16 trillion, up 61 percent from the previous year. In the current account, which reflects the national net income, the proportion of RMB-dominated imports and exports went from 5.5 percent in 2011 to 11.7 percent in 2013. In the capital account, which reflects ownership of investments, in 2013 RMB-denominated direct investments in China increased by about 60 percent year-on-year while China’s outbound RMB-denominated investments increased by 130 percent. That means that the RMB has found increased acceptance by overseas clients.

Over 222 countries and regions now use the RMB in collection and payments. The products covered now include bank assets, liabilities and intermediate business such as deposits, loans, insurance, clearing, fund transactions, wealth management and bonds underwriting.

The rise of cross-border RMB settlements has boosted the currency’s international status. According to the Bank for International Settlements (BIS), the RMB is now one of the 10 most traded currencies. It climbed from the 17th in global foreign exchange market turnover in 2010 to ninth in 2013, with average daily turnover increasing 2.5 times.

According to the latest statistics from the Society for Worldwide Interbank Financial Telecommunication (SWIFT), by the end of 2013 the RMB accounted for 1.13 percent of international payments, almost twice the level at the begining of the year. Meanwhile, China has strengthened its monetary cooperation with the rest of the world. It has signed currency swap agreements with 23 countries and regions, with the total value exceeding RMB 2.5 trillion. Several countries in Southeast Asia, Eastern Europe and Africa have taken or considered taking RMB as their official reserve currency.

Developing Offshore Market

RMB internationalization can’t be achieved without the support of offshore markets, which have historically played a key role in the creation of new world currencies. These can be distinguished into two parallel markets: the cisborder offshore market and the overseas offshore market. When, for example, a U.S. dollar offshore market was formed in London, the U.S. also promoted the development of a cisborder offshore market – International Banking Facility (IBF).

For RMB, there will also be cisborder and overseas offshore markets. One of the goals of establishing China (Shanghai) Pilot Free Trade Zone is to promote the formation and development of a cisborder offshore RMB market. However, since the RMB is not completely convertible under the capital account, it is necessary to establish the first offshore RMB market in Hong Kong.

In 2004 the RMB entered circulation in Hong Kong. After a pilot program the RMB has been increasingly used in trade settlements between China’s mainland and Hong Kong. In February, 2010, the Hong Kong Monetary Authority adjusted policy to loosen control over the RMB. In July of the same year, the People’s Bank of China and the Bank of China (Hong Kong) Limited signed a settlement agreement on the clearing of RMB business in Hong Kong, again expanding the scale of offshore RMB business. Thereafter the offshore RMB market in Hong Kong has entered a period of rapid growth.

By the end of 2013, RMB deposits in Hong Kong reached RMB 86.05 billion, accounting for over half of the currency’s overseas stock. Meanwhile, the emergence of RMB loan, bond and derivatives markets have further boosted the construction of the offshore RMB market in Hong Kong. In addition, international financial centers such as Singapore, London, Paris and Frankfurt also make their due contributions to the development of offshore RMB markets. From a long-term perspective, more offshore RMB markets can be expected in major global financial centers.

|

|

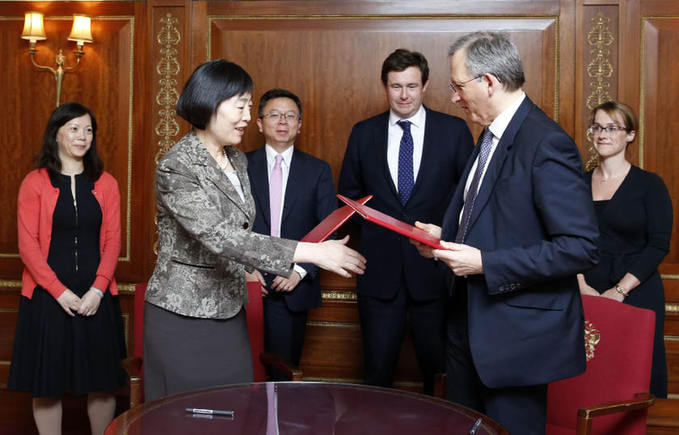

Deputy Governor of the People’s Bank of China Madame Hu Xiaolian (second left) and Deputy Governor of the Bank of England Jon Cunliffe (second right) sign a Memorandum of Understanding on RMB Clearing and Settlement in London on March 31, 2014. |